RULE 13

Special Rules for Directors, Partners, or Auditors

Introduction

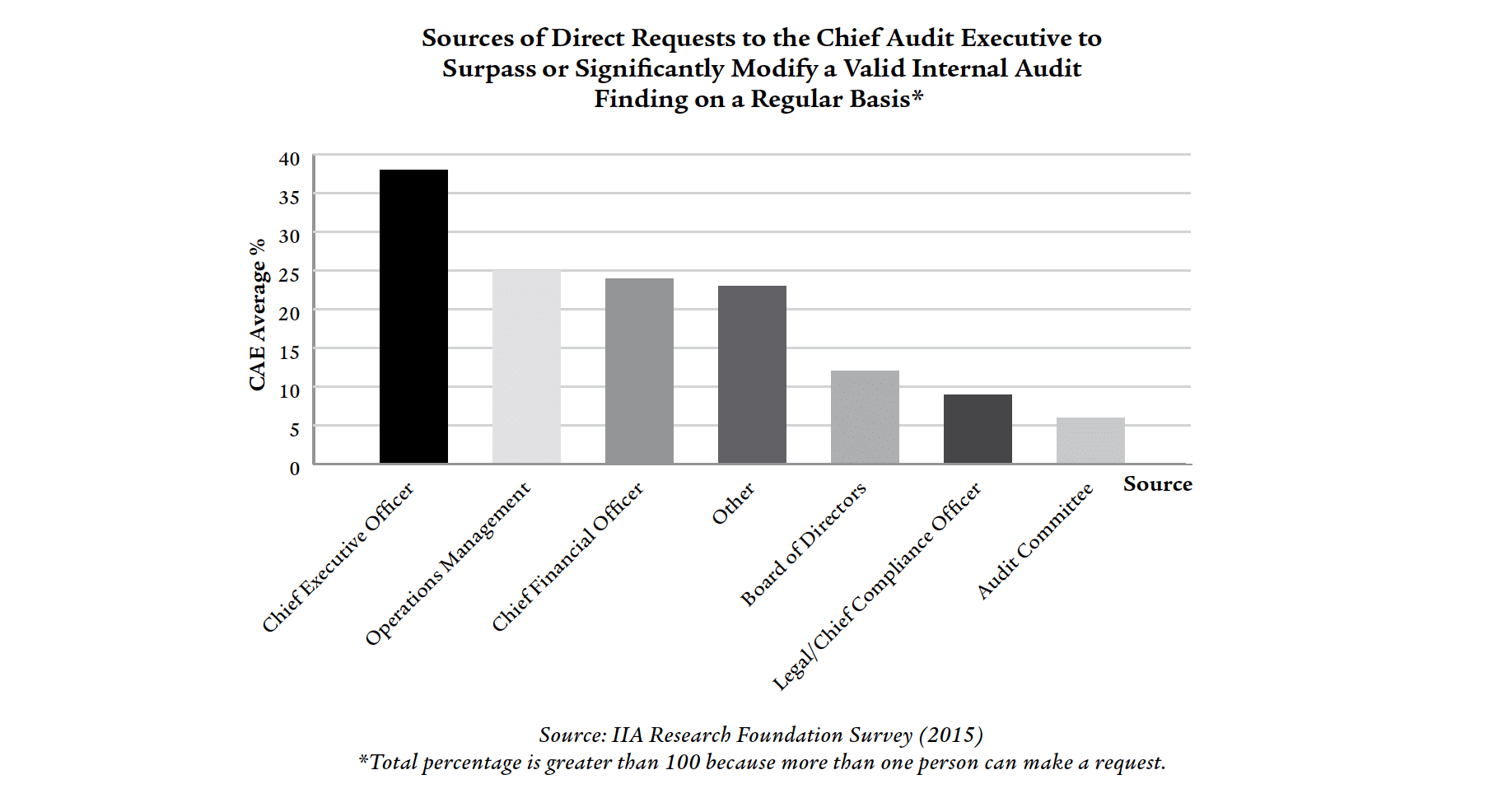

Directors, partners, and auditors are often in the best positions to become whistleblowers. They are more likely to be made aware of corrupt practices and are able to gain the trust of other employees. Auditors may discover misconduct in their reports, or better yet, be asked to cover it up by the C-Suite. A 2015 report by the Institute of Internal Auditors found direct evidence of chief auditors being asked to modify audit results, asked to not perform audits in certain high-risk areas, and asked to produce audits solely for the purpose of employee retaliation. Rules differ under each of the whistleblower laws, but agencies acknowledge that for how well-placed these employees are, they should act as “recruitment-in-place” style whistleblowers. Read the Rule for the five tips offered to those reporting as a director, partner, or auditor.

Practice Tips

- The SEC regulation on auditor, compliance, and director eligibility for rewards is set forth at 17 C.F.R. § 240.21F-4(b)(4)(iii) and (v).

- The Commodity Futures Trading Commission’s regulation on auditor, compliance, and director eligibility is set forth at 17 C.F.R. § 165.2(g)(4), (5), and (7).

- Best practice: If you are a compliance official, director, attorney, or auditor, file your reward claim 120 days after the company was alerted to the violation.

Resources

The problems faced by auditors and compliance officials are well documented.

- Institute for Internal Auditors, “Political Pressure Intense on Internal Audit: IIA Research Report Reveals Pervasive Efforts to Influence Internal Audit Findings,” press release (Mar. 10, 2015).

The Institute for Internal Auditors survey of auditors is known as the Global Internal Audit Common Body of Knowledge. The survey’s results were analyzed in:

- The Politics of Internal Auditing by Patricia Miller and Larry Rittenberg, published by the IIA Research Foundation, Altamonte Springs, Florida (2015).

See also:

- Ethics and Pressure: Balancing the Internal Audit Profession by Larry Rittenberg (The IIA Research Foundation, 2016).

SEC decisions granting awards to compliance officials:

- SEC Press Release 2014-180 (Aug. 29, 2014) (first compliance official obtains monetary reward)

- SEC Press Release 2015-73 (Apr. 22, 2015) (compliance official awarded $1.5 million)

Requirement that publicly traded companies have a program to accept confidential employee concerns regarding questionable accounting and auditing practices is codified at:

The development of the SEC’s rule on director, partner, attorney, and compliance official coverage is discussed at:

- “Speech by Chairman Mary L. Schapiro,” U.S. Securities and Exchange Commission, Washington, DC (May 25, 2011) (SEC Whistleblower Program)

- Stephen Kohn, “The SEC’s Final Whistleblower Rules and Their Impact on Internal Compliance,” West Law Publishing (Oct. 2011) (rights of compliance officials to blow the whistle)

Whether auditors, compliance officials, or employees whose duties require them to perform compliance functions are protected against retaliation remains a controversial topic. However the two decisions issued by the Supreme Court demonstrate that without specific statutory coverage, internal disclosures by these classes of employees may be unprotected.

See Supreme Court decisions finding internal whistleblowing not protected under the Dodd-Frank Act and First Amendment:

- Digital Realty Trust v. Somers, 138 S.Ct. 767 (2018);

- Garcetti v. Ceballos, 547 U.S. 410 (2006)

However, a wealth of cases decided before Digital and Garcetti explained the fact that whistleblowers often used internal reporting processes and should deserve protection:

- Phillips v. Interior Board of Mine Op., 500 F.2d 772 (D.C. Cir. 1974)

- Mackowiak v. University Nuclear Systems, 735 F.2d 1159 (9th Cir. 1984)

- Kansas Gas & Electric v. Brock, 780 F.2d 1505 (10th Cir. 1985)

- Passaic Valley Sewerage Commissioners v. DOL, 992 F.2d 474 (3rd Cir. 1993)

- U.S. ex rel. Yesudian v. Howard University, 153 F.3d 731 (D.C. Cir. 1998)

- Bechtel v. DOL, 50 F.3d 926 (11th Cir. 1995)

- Poulos v. Ambassador Fuel Oil Co., 86-Clean Air Act Case No. 1 (Apr. 27, 1987)

Pre-Digital cases discussing whether compliance officials, auditors, and attorneys are covered under anti-retaliation laws:

- Brown & Root v. Donovan, 747 F2d 1029 (5th Cir. 1984) (auditor not protected), but the case was reversed in Willy v. ARB, 423 F.3d 483 (5th Cir.) (an attorney protected in Willy)

- Kansas Gas & Elec. v. Brock, 780 F.2d 1505 (10th Cir. 1985) (quality assurance inspector protected)

- Mackowiak v. University Nuclear, 735 F.2d 1159 (9th Cir. 1984) (inspector protected)

- Van Asdale v. International Game Tech., 577 F.3d 989 (9th Cir.) (attorney protected)

Cases

- Brown & Root v. Donovan, 747 F2d 1029. – auditor not protected.

- Kansas Gas & Elec. v. Brock, 780 F.2d 1505 – auditor protected.

- Mackowiak v. University Nuclear, 735 F.2d 1159 – auditor protected.

- Van Asdale v. International Game Tech., 577 F.3d 989 – Attorney protected.

- Willy v. ARB, 423 F.3d 483 – Attorney protected.

Quick Links

- 15 USC § 78u-6

- 17 C.F.R. § 240.21F-1 through F-17

- 17 C.F.R. § 249.1800 & 1801

- 15 U.S. Code § 78j–1 – Audit requirements (Required under the Sarbanes-Oxley Act of 2002).

- 2011 Compliance Rules Federal Sentencing Guide, Chapter Eight, Part B(2) – Effective Compliance and Ethics Program

- 48 CFR Ch. 1 – Subpart 3.9 Whistleblower Protections for Contractor Employees

- 48 CFR Ch. 1 – Subpart 3.10 Contractor Code of Business Ethics and Conduct

- 48 CFR Ch. 1 – 52.203–13 Contractor Code of Business Ethics and Conduct

- 17 C.F.R. 205 – Standards of Professional Conduct for Attorneys

- Brown & Root v. Donovan, 747 F2d 1029. – auditor not protected.

- Kansas Gas & Elec. v. Brock, 780 F.2d 1505 – auditor protected.

- Mackowiak v. University Nuclear, 735 F.2d 1159 – auditor protected.

- Van Asdale v. International Game Tech., 577 F.3d 989 – Attorney protected.

- Willy v. ARB, 423 F.3d 483 – Attorney protected.

- In the Matter of Adriana Koeck, No. 14-BD-061 (2014)

- SEC Awards $1.6 Million to Compliance Officer for Protecting Investors

- Stephen Kohn, “The SEC’s Final Whistleblower Rules & Their Impact on Internal Compliance” (West Law Publishing, Oct. 2011)

- Compliance Professional Awarded $300,000 by SEC

- Speech by SEC Chairman Mary L. Schapiro: Opening Statement at SEC Open Meeting — Whistleblower Program (May 25, 2011)

- SEC Press Release 2015-73 (April 22, 2015) (compliance official awarded $1.5 million)

Compliance professionals are on the front line of uncovering and reporting fraud. However, the pressure to change audit reports came from the top.

- Transforming Compliance: Emerging Paradigms for Boards, Management, Compliance Officers, and Government, Michael D. Greenberg, Rand Center for Corporate Ethics and Governance (2014)

- Culture, Compliance, and the C-Suite: How Executives, Boards, and Policymakers Can Better Safeguard Against Misconduct at the Top,Michael D. Greenberg, Rand Center for Corporate Ethics and Governance (2013)

- For Whom the Whistle Blows: Advancing Corporate Compliance and integrity efforts in the era of dodd-frank, Rand Center for Corporate Ethics and GovernanceMichael D. Greenberg, Rand Center for Corporate Ethics and Governance (2011)

- Avoiding The Perils and Pitfalls of Internal Corporate Investigations: Proper Use of Upjohn Warnings, Jeffrey Eglash et al. (2010)

- Impact of Qui Tam Laws on Internal Compliance: A Report to the Securities and Exchange Commission, National Whistleblower Center (2010)

- Directors as Guardians of Compliance and Ethics Within the Corporate Citadel: What the Policy Community Should Know, Michael D. Greenberg, Rand Center for Corporate Ethics and Governance (2010)

- From Enron to Madoff: Why Many Corporate Compliance and Ethics Programs Are Positioned for Failure, Donna Boehme (2009)

- Redefining the Relationship of the General Counsel and Chief Compliance Officer, Michael Volkov, CEO, The Volkov Law Group

Frequently Asked Questions

Related Rules

Order Your Copy Today!

All purchases or donations proceeds go to support the National Whistleblower Center, a 501(c)(3) non-profit organization dedicated to supporting whistleblowers.

Shipping is to the United States Only

For international orders, please contact [email protected].